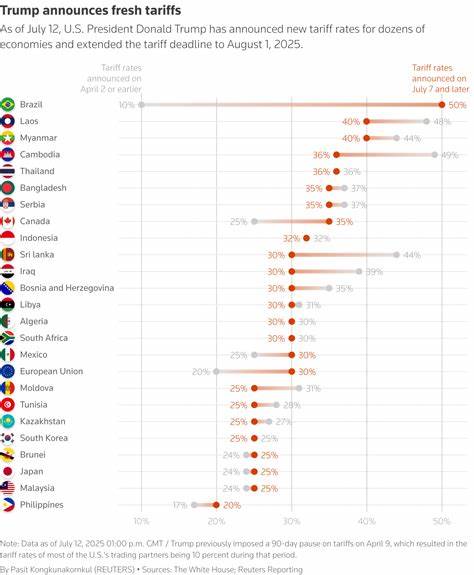

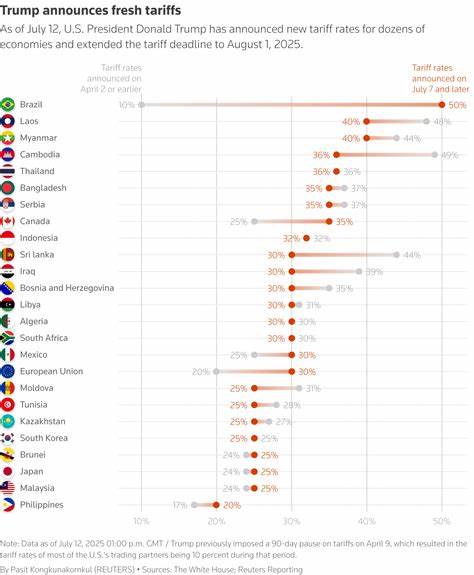

美国梦长期以来一直以拥有自己的住房作为核心象征,这不仅代表着经济稳定,也象征着社会地位和未来发展的希望。然而,随着时代的演变,传统金融体系在评估财富和信用资质时显得越发局限,尤其对于那些依赖数字资产积累财富的新兴群体而言,这一体系显然存在壁垒。近日,美国联邦住房金融署(FHFA)决定将加密资产纳入房屋贷款评估体系,这一政策转折被视为数字财富正逐渐渗透到美国经济的根基,进而重塑美国梦的内涵。加密货币到底为美国梦带来了怎样的变革?它是如何影响传统金融审慎观念,并为更多人开启购房大门的?带着这些疑问,我们深入剖析这一趋势背后的经济与社会逻辑。过去,房屋贷款资质审核主要依赖于传统的收入证明、资产评估、信用评级以及固定工作证明。对于拥有稳定工资单的雇员来说,这一体系较为有效,能够在一定程度上保证贷款方的风险控制。

然而,随着数字经济和自由职业的兴起,越来越多的人通过加密货币、区块链技术以及数字资产积累财富,他们的资产并不表现为传统的银行存款或者固定投资,而是存在于去中心化的区块链钱包中。由于缺乏标准化的评估体系,传统金融机构普遍对这部分资产持怀疑态度,甚至不将其视为“真实财富”,这使得很多数字资产持有人在申请房贷时处于不利地位。值得注意的是,2025年7月,FHFA宣布将允许房贷机构如房利美和房地美在审核抵押贷款时认可加密资产。这表明数字财富不再是边缘经济体系的专属特权,而是被正式纳入传统金融框架内。这不仅是对加密资产价值的首次官方认可,更是经济体系迈向包容与多元化的重要里程碑。这次政策调整的意义不仅体现在贷款门槛的降低上,更深层次地体现出美国梦的定义开始进化。

财富不再仅仅是存在银行账单上的数字,也不仅限于传统的存款和投资组合,而是涵盖了数字世界中的资产形态。这一改变将为那些依赖数字经济创业、自由职业者、区块链开发者甚至是加密货币投资者提供更多机会,让他们的财富能够转化为现实的住房和生活保障。根据2024年的报告,越来越多的购房者选择将加密货币作为首付资金,这一比例从2019年的5%飙升至12%。与此同时,不少企业也开始打造能够将数字资产用作贷款抵押的金融产品,甚至帮助用户在不引发资本利得税的情况下进行数字资产借贷。这种新型的金融服务不仅丰富了市场选择,也降低了数字资产流动性不足带来的困扰,为购房者打开了新的融资渠道。批评者对于将高波动性的加密资产纳入房贷评估持有担忧,认为这可能给贷款机构带来更大的信用风险。

事实上,传统金融危机的大部分问题并非来自于财富的波动性,而是过度杠杆、信息不透明和复杂的金融衍生品操作。相反,加密货币利用区块链技术的透明度,使得资产余额和交易在网络上可查,提供了更为公开和可信的资产证明。智能合约也防止了造假和数据篡改。由此,新兴的去中心化金融体系(DeFi)通过开放和透明的机制,有望降低信息不对称和信用风险,这与过去影子银行体系中的隐患形成鲜明对比。Beyond finance, the integration of crypto assets into mortgage qualification represents a broader concept of freedom and financial inclusion in the 21st century. It challenges the idea that wealth is solely accumulated through traditional pathways like salary or savings. Instead, it validates the efforts of risk-taking entrepreneurs and digital pioneers who built wealth without the gatekeepers of the old economy, thus democratizing access to homeownership. This shift also inspires new financial behaviors wherein homes are no longer just assets but also platforms. Some individuals leverage their real estate equity to invest in digital assets, flipping the conventional asset-accumulation model on its head. While this introduces additional financial risks, it underscores the need for innovative, balanced regulation that nurtures innovation without compromising consumer protection. The emerging blueprint of the American Dream reflects a hybrid world where ownership bridges physical and digital realms, and creditworthiness encompasses on-chain transparency alongside traditional documentation. Housing markets must adapt to these changes to remain relevant and accessible to a broad demographic. For millions of digital investors and innovators, policy shifts like the FHFA’s represent a critical bridge connecting their digital achievements to tangible life goals. The old maxim “location, location, location” now extends beyond physical neighborhoods to encompass online, decentralized, and transparent digital assets. Ultimately, the incorporation of cryptocurrency into mortgage lending is not a threat to traditional homeownership but a catalyst for its reinvention. It signals an evolution in societal values, embracing a more inclusive definition of wealth and success applicable in today’s interconnected digital economy. As this transformation unfolds, the true promise of the American Dream—to provide stability, opportunity, and upward mobility—stands to be renewed and expanded for a new generation of homeowners. In conclusion, the recognition of digital assets by regulatory bodies marks a pivotal point in the convergence of traditional finance with cutting-edge technology. It opens up a pathway for diversified wealth holders to engage meaningfully in the housing market, reflecting a broader trend toward financial integration and modernization. The renovation of the American Dream through crypto is a testament to adaptive economic systems that value innovation, transparency, and inclusivity. For those navigating the intersections of real estate and digital wealth, the future holds unprecedented possibilities where owning a home and possessing digital assets coexist and complement each other in the pursuit of prosperity and freedom.。